Join 1,500+ businesses that rely on MSA to Start, Manage, and Grow their business in China.

Share this article

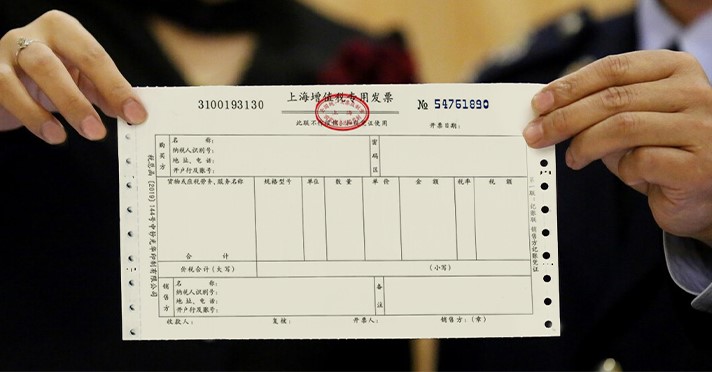

The concept of “Fapiao” (发票) in China is central to the country’s tax administration system. Fapiao are official invoices issued by the Chinese tax authorities that serve as proof of purchase for goods and services. They are critical to China’s efforts to document business transactions and monitor tax compliance. Using fapiao has been an integral part of the government’s strategy to modernize tax collection, reduce evasion, and increase transparency in the economy.

Recently, China has been undergoing a technological evolution of its VAT administration, including reforms to the Fapiao system. Implementing electronic Fapiao aims to streamline the process, making it easier for businesses to comply with regulations and for the tax authorities to track transactions efficiently.

In this guide we explain how the Fapiao system works and what businesses in China need to do to ensure compliance with the system.

A fapiao is a business voucher issued and received by all parties purchasing and selling goods or services. The Fapiao is the original document accounting for a cost, an expense, or revenue. In essence, the fapiao has three purposes:

1. Individuals use a Fapiao to reimburse business expenses;

2. Companies use Fapiao for accounting purposes and tax deductions; and

3. The Chinese authorities use Fapiao to track transactions for tax purposes and to prevent tax evasion.

The Fapiao system is central to understanding China’s tax infrastructure. It is integral to the nation’s compliance and transparency in collecting Value-Added Tax (VAT).

There are three types of Fapiao:

These are used for standard sales transactions and services. They are issued to both individuals and businesses for accounting and expense tracking.

These are not eligible for VAT deduction and businesses cannot use General VAT Fapiao to claim input VAT credits. They are primarily used for recording business expenses.

They are used primarily by small-scale VAT taxpayers and for certain goods or services specified by the tax law. The information on a General VAT Fapiao only records a few necessary transaction details.

These are used specifically for transactions involving VAT-registered businesses. They are essential for businesses to claim input VAT credits and offset their output VAT liabilities.

They contain detailed information such as the taxpayer’s name, the transaction amount, and the applicable tax rate. These fapiao can only be issued by businesses that are general VAT taxpayers and are authorized by the tax bureau to issue such documents. Receipt of a special VAT fapiao allows businesses to deduct the input tax from their output tax obligations.

China’s tax system is evolving with technology, and electronic fapiao, or e-fapiao, streamlines the tax reporting process. E-fapiao serve the same legal function as their paper counterparts but are created, transmitted, and stored digitally. This modern approach reduces the use of paper, minimizes fraud, and enhances the efficiency of tax administration.

Navigating the various types of fapiao can help one understand how VAT is implemented and managed within China’s complex tax system.

The State Administration of Tax (SAT) oversees the printing, distribution, and administration of Fapiao in China. The central system the SAT uses to administer Fapiao is called the “Golden Tax System”.

When businesses want to issue official invoices in China, they must first obtain empty sheets of Fapiao paper at the tax bureau, with only a range of Fapiao numbers explicitly associated with the company’s current batch of Fapiao. Subsequently, companies must print the fapiao sheets with a particular printer linked to the tax system. Companies will have a device, typically a USB stick, called the “Golden Tax Device” (see image below) to log into the printer program, which identifies the company and is connected to the tax system. The system will automatically indicate the following Fapiao number that can be used for printing and should be placed in the printer. The authorities allow companies to choose the category themselves; however, according to PRC legislation, you cannot perform business outside your scope.

Therefore, it is essential that the category chosen is in line with the company’s business scope, and the company has the responsibility to act by the law.

The old Golden Tax Device (left) and the new version (right).

Because the printer and Golden Tax Device identify the company and link directly with the tax system, a transaction is recorded in the tax bureau’s records. VAT is due upon printing a fapiao and is payable the following month.

After a customer receives a fapiao, he/she must log in to their tax system and use the tax program to verify the transaction. After that, the tax will be deductible, and the deduction will be applied in the next month against the tax payable.

The fapiao system is also linked to the VAT declaration system. When companies file figures with the monthly VAT declaration inconsistent with the issued fapiaos, the declaration system will notify the company and prohibit the declaration process. Subsequently, the company will not be able to issue fapiaos until the discrepancy is resolved. The physical fapiao must be kept in the company’s records, as companies must legally maintain physical records for 30 years.

Since the literal translation of fapiao is “invoice” and there is no comparable document in most other countries, the fapiao may sometimes confuse individuals from overseas. In China, some invoices resemble the commercial ones used in different countries worldwide. For example, there are international invoices (账单) and receipts (收据or 小票). However, although these invoices document the amount of goods/services provided and the price, they are not official tax invoices with legal validity and do not determine when taxes are due. In China, these invoices differ from the fapiao and can be viewed as a payment notice comparable to a proforma invoice.

In China, the issuance and regulation of Fapiao receipts are paramount to ensuring compliance with tax laws and preventing tax evasion. This section will explore the legal ramifications of Fapiao misuse and the regulatory environment that governs businesses’ proper issuance.

Tax evasion in China is a serious offense, and the legal implications for misuse of Fapiao can be severe. The tax authorities vigilantly monitor the issuance of Fapiao to enforce tax laws and maintain government revenue. The Chinese government mandates using Fapiao to document sales transactions that involve providing goods and services. When businesses fail to issue or incorrectly issue Fapiao, they are subject to penalties by the local tax bureau. Individuals or entities caught trading in counterfeit or illegal Fapiao receipts face stringent legal consequences, including fines and imprisonment.

The regulatory framework for Fapiao is managed by the tax bureau and is intended to reinforce compliance with China’s tax laws. Regulations require companies to purchase Fapiao booklets from the tax authorities before issuing them to customers. Each Fapiao has unique identification numbers, enabling tax authorities to track sales transactions and tax payments accurately. Moreover, recent efforts to digitize the Fapiao system aim to increase the efficiency of tax collection and minimize the potential for fraud. Businesses need to adhere to these regulations and maintain transparent records of their financial transactions to remain compliant with the legal and tax compliance framework established by the Chinese government.

In China, the Fapiao is an official invoice system used for tax purposes, which is critical for businesses and individuals looking to claim tax deductions. The State Taxation Administration (STA) administers the system, which ensures tax compliance and enables taxpayers to deduct certain expenses from their taxable income.

To claim a tax deduction, taxpayers in China must ensure their expenditures are eligible under the STA’s regulations. Expenses that typically qualify include those related to business operations, such as purchasing goods, business travel, or utilities that incur Input VAT. Only expenditures with an adequately issued Fapiao can be used for tax deduction.

The validation process involves a thorough check to ensure the Fapiao is properly issued with accurate details. Taxpayers must ensure their fapiao includes:

The STA completes verification, cross-referencing the details on the fapiao with its records. Businesses and individuals must retain these invoices for the stipulated period as they serve as proof of eligible expenditures for claiming tax deductions.

Failure to produce a verifiable Fapiao when requested by the STA may result in the denial of the tax deduction claim. Therefore, strict compliance with Fapiao regulations is essential for successful tax deduction claims in China.

The fapiao system, integral to China’s taxation, exhibits significant variances across different regions and has been subject to several pilot programs aimed at modernization and reform.

In China, the Fapiao invoice system functions differently across provinces and cities, reflecting local administrative approaches to taxation. For instance, as China’s major economic hubs, Beijing and Shanghai have more sophisticated requirements for issuing these invoices, often demanding detailed documentation for tax deduction purposes. By contrast, other regions such as Anhui or Sichuan have less stringent procedures, though compliance remains a priority for businesses and individuals. The variation often reflects the economic complexity of the region, with more developed areas such as Shenzhen and Dalian possibly adopting stricter controls to reflect their higher volume of business transactions.

Numerous pilot programs have been introduced across China to test reforms in issuing and managing fapiao. Notable pilot locations include Tianjin, Chongqing, and parts of Shanghai, where digital fapiao systems are being trialed. These programs endeavor to increase efficiency and decrease fraud. Shenzhen introduced a lottery system linked to fapiao, incentivizing consumers to request and retain their invoices, reinforcing its role in tracking economic activity and assisting in tax collection efforts.

VAT taxpayers in China are categorized as VAT General and VAT small-scale taxpayers. Businesses with annual taxable sales exceeding the pre-determined ceiling for small-scale taxpayers must apply for General VAT taxpayer status.

Generally the income threshold for General VAT tax payer is RMB 5 million. Businesses with annual sales below the ceiling or those that are newly established may voluntarily choose to apply for General VAT taxpayer status, provided that they keep legitimate and accurate bookkeeping.

The VAT rates for General VAT taxpayers are 6%, 9%, and 13%. Small-scale taxpayers are subject to a VAT rate of 3% (currently 1% for 2020 and 2021 in light of COVID-19 support measures) but cannot deduct input VAT from output VAT. In the past, small-scale taxpayers could not print VAT invoices by themselves (and instead had to visit the tax office to print them). Nowadays, they can also apply to the tax office to print fapiaos.

Through our experience working with hundreds of international businesses in China, here are our tips based on some of the most common mistakes made by those who are not used to the system.

It is recommended to provide a Fapiao to customers only after receiving a payment. The moment a Fapiao is printed, the obligation to pay VAT arises in the current period. If the seller has not received payment from the buyer in the current period, this may create a cash flow problem.

Moreover, it is essential to note that canceling a Fapiao is complicated and time-consuming. The difficulty in canceling a Fapiao depends on whether the cancellation will be done in the same accounting period as the moment of issuance and whether the customer has already verified the Fapiao. If a customer has already verified the Fapiao, the customer must apply to cancel. Therefore, it is even more advisable to only provide Fapiao to customers after receiving payment.

Fapiaos are not issued by default, and therefore, it is the customer’s responsibility to request to receive a Fapiao. On the other hand, by Chinese tax law, you are obligated to issue a Fapiao when services have been rendered or ownership of goods has been transferred. This means that refusal to issue a Fapiao is illegal in these circumstances, and any uncooperative company can be reported to the local tax authority.

The number of Fapiaos a company can issue and the maximum monetary amount per Fapiao is subject to a quota set by the local tax bureau and differs considerably per province-, city- and district level, as well as the in-charge tax officer. Additionally, unwritten requirements will generally influence the tax authorities’ judgment on the quantity and value of Fapiao to be issued to a company, such as the company’s registered capital, office size, and number of employees.

A fapiao (or 发票 in Chinese) is an official Chinese invoice used to recognize expenses for accounting purposes, track transactions for tax purposes, and prevent tax evasion. It is important to note that although you may encounter other commercial or proforma invoices in China, they fulfill a different function than the Fapiao. Therefore, it is recommended that all foreign businesses in China understand the impact the fapiao has on the company’s tax and financial position.

Due to the particulars of the Chinese invoicing system, invoicing in China is more complex and requires a greater workload compared to many other countries. For this reason, many small- and medium-sized foreign-invested enterprises in China elect to outsource the Fapiao procedures to a third party while maintaining control over the issuance of payment notices and payment collection. For any further questions about Fapiao, please do not hesitate to contact us.